{kind=link}

This surge is being driven by robust demand in advanced technology segments such as electronic warfare systems, C4 (command, control, communications, computers and intelligence) systems, and aerospace equipment and components. These areas are increasingly becoming the backbone of order book expansion for private players, offering strong revenue visibility and growth momentum.

The shift in market dynamics reflects the growing competitiveness and capability of the private sector, which now contributes nearly half of the defence industry’s revenues among Crisil-rated companies.

Backed by government initiatives like Atmanirbhar Bharat, the Defence Acquisition Policy, and the Defence Production and Export Promotion Strategy, private firms are capitalising on the push for indigenisation and reduced dependence on imports. These policies, combined with increased capital outlays and sustained geopolitical tensions, have led to a steady rise in defence spending and domestic procurement.

“The rise in private sector participation is supported by investments in R&D and capex, which have enhanced technical capabilities and enabled players to secure larger and more complex orders,” said Jayashree Nandakumar, Director, Crisil Ratings.

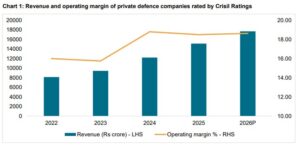

Crisil Ratings estimates that revenue for private defence players will grow at 16–18% in fiscal 2026, following a ~20% compound annual growth rate (CAGR) recorded between fiscals 2022 and 2025. Operating margins are expected to remain stable in the 18–19% range, aided by price escalation clauses in contracts and the overall scale of growth. Companies have been investing heavily in capacity expansion and research and development, enhancing their ability to win and execute large, complex contracts.

To support the anticipated growth, private defence firms are expected to invest around ₹1,000 crore each in capital expenditure and incremental working capital during the current fiscal.

However, thanks to strong internal accruals and equity infusions of nearly ₹3,600 crore over the past three years—primarily through IPOs and private equity—these investments are not likely to exert pressure on debt levels.

“Debt levels are unlikely to increase this fiscal, as most funding will come from internal resources,” said Sajesh K V, Associate Director, Crisil Ratings.

As a result, key financial indicators remain healthy, with the total outside liabilities to tangible net worth (TOL/TNW) ratio expected to stay stable at around 1.15 times as of March 2026, and the interest coverage ratio projected to improve to 5.5 times, up from 5.2 times in fiscal 2025.

Despite the positive outlook, Crisil notes that certain risks warrant close monitoring, including potential shifts in defence policy, semiconductor supply chain challenges, and any elongation in the working capital cycle.