{kind=link}

Despite the overall slump, the office segment remained resilient, drawing $706 million in PE investments—a 22% increase from the same period last year.

The data signals a shift in global investor sentiment, influenced by high interest rates, tighter liquidity, and a stronger focus on post-tax, risk-adjusted returns. “The current global economic environment marked by persistent inflation and tighter monetary conditions has led many Western funds to take a cautious, wait-and-watch stance,” said Shishir Baijal, Chairman and Managing Director of Knight Frank India.

Office and residential lead

The residential sector emerged as the second-largest recipient of PE capital, attracting $500 million. The retail segment also showed signs of recovery, drawing $481 million through two large-scale deals. In contrast, warehousing, which had been a consistent magnet for PE funding since 2018, attracted just $50 million, marking its weakest performance in seven years.

Changing capital composition and investor base

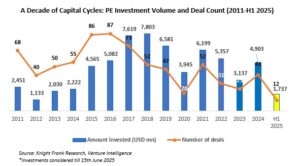

The report highlights a structural evolution in capital flows. Western institutional investments retreated, hindered by the narrowing India-U.S. yield differential, rupee depreciation—from ₹83.1 in December 2023 to ₹85.6 per USD in mid-2025—and India’s 12.5% long-term capital gains tax.

This vacuum has been increasingly filled by domestic players. Indian institutions contributed 25% of total PE investments in H1 2025, a notable jump from their 11% average between 2011 and 2020, driven by deeper local capital pools, enhanced regulatory frameworks, and growing institutional capabilities.

Regional trends: South India gains momentum

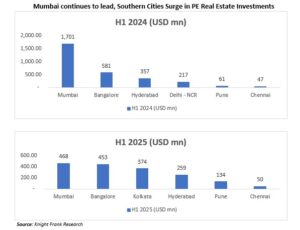

Mumbai topped the list of cities with the highest PE inflows at $468 million, followed closely by Bengaluru at $453 million. Other notable destinations included Kolkata ($374 million), Hyderabad ($259 million), Pune ($134 million), and Chennai ($50 million). Together, cities in South India accounted for over 44% of total investments, underlining a growing regional shift in investor focus.

Mumbai topped the list of cities with the highest PE inflows at $468 million, followed closely by Bengaluru at $453 million. Other notable destinations included Kolkata ($374 million), Hyderabad ($259 million), Pune ($134 million), and Chennai ($50 million). Together, cities in South India accounted for over 44% of total investments, underlining a growing regional shift in investor focus.

Despite the downturn in PE activity, long-term optimism remains. Baijal noted that India’s commercial real estate market benefits from a “return to office” trend, robust absorption rates, and rising rental values. These fundamentals, alongside sustained economic momentum and improving regulatory clarity, could encourage global capital to return once macroeconomic conditions stabilize.