{kind=link}

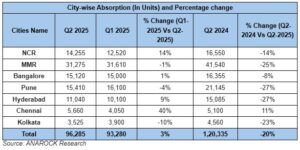

Approximately 96,285 housing units were sold in Q2 2025, down from 1,20,335 units sold during the same period last year. In comparison to Q1 2025, which recorded sales of 93,280 units, Q2 showed a slight improvement.

Among the top seven cities, Chennai stood out with an 11% annual increase in sales, clocking around 5,660 units in Q2 2025 versus 5,100 in Q2 2024. The city also saw a 40% Q-o-Q surge from Q1 2025. Mumbai Metropolitan Region (MMR) and Pune continued to dominate in terms of volume, jointly accounting for 48% of total housing sales, with 31,275 and 15,410 units sold respectively.

New residential launches saw a 16% decline Y-o-Y, falling from approximately 1,17,165 units in Q2 2024 to about 98,625 units in Q2 2025. On a quarterly basis, new launches dipped marginally by 1%. Despite the drop, MMR and the National Capital Region (NCR) led fresh supply additions, together contributing 48% of the total. Notably, NCR recorded a 69% surge in new supply Q-o-Q and a 10% annual increase, indicating rising developer confidence in the region.

Chennai also witnessed a significant 65% Y-o-Y jump in new project launches, bucking the trend of deceleration seen in most other cities.

High-end residential segments continue to dominate new launches. Luxury and ultra-luxury homes (priced above ₹1.5 crore) made up 46% of the new supply in Q2 2025. Mid-range (₹40–80 lakh) and premium (₹80 lakh–₹1.5 crore) homes each held a 21% share, while affordable housing (below ₹40 lakh) remained subdued at just 12%.

High-end residential segments continue to dominate new launches. Luxury and ultra-luxury homes (priced above ₹1.5 crore) made up 46% of the new supply in Q2 2025. Mid-range (₹40–80 lakh) and premium (₹80 lakh–₹1.5 crore) homes each held a 21% share, while affordable housing (below ₹40 lakh) remained subdued at just 12%.

Average property prices across the top seven cities rose by 11% annually, though the quarterly growth was just 1%. NCR led with a substantial 27% Y-o-Y price rise, followed by Bengaluru (12%) and Hyderabad (11%).

Anuj Puri, Chairman of ANAROCK Group, described Q2 2025 as a turbulent period for India’s housing market, heavily influenced by geopolitical unrest and military actions both domestically and internationally. “The heightened tensions created a war-like environment that led many homebuyers to adopt a wait-and-watch approach,” he said, noting that this added to the pressure from already high property prices seen over the last two years.

“While sales across the top seven cities dropped 20% year-on-year, the 3% quarter-on-quarter increase points to a potential revival,” he stated. “Easing home loan rates and relatively stable pricing by developers could pave the way for a stronger housing market in the upcoming quarters.”

Unsold housing inventory across the top cities stood at approximately 5.62 lakh units at the end of Q2 2025, showing a marginal increase from 5.60 lakh in Q1 2025. On a yearly basis, however, unsold stock dropped by 3%. Pune led the improvement with a significant 15% Y-o-Y reduction in unsold inventory, from 94,770 units in Q2 2024 to 80,240 units by Q2 2025.