{kind=link}

With both domestic and export demand on the upswing, combined with favorable government policies and monetary easing, industry volumes are projected to grow by 8–9% in FY26—finally crossing the pre-COVID peak achieved in FY19.

Over the past three fiscal years, the industry has shown a steady recovery, recording wholesale volume growth of 8% in FY23, 10% in FY24, and 11% in FY25. In FY25, total wholesale volumes reached 23.81 million units—just shy of the FY19 high. This growth was led by a 21% rebound in exports and a 9% rise in domestic sales, reflecting broad-based recovery.

Rural markets lead the charge

Rural India played a crucial role in this resurgence, accounting for 58.3% of total retail registrations in FY25—up from 57.9% in the previous year. Improved rural sentiment, coupled with steady urban demand and stabilizing export markets, propelled the sector’s growth.

“The two-wheeler industry is set to vroom past pre-COVID levels in FY26 with volume growth of 8–9%, aided by accelerating export volumes at 12–14% and stable domestic growth of 6–8%,” said Madhusudhan Goswami, Assistant Director at CareEdge Ratings.

“Supportive factors include easing inflation, improved rural sentiment, and increased affordability due to income tax rebates and monetary easing.”

The Reserve Bank of India has cut interest rates by 100 basis points since February 2025, including a 50 bps cut in June—boosting credit availability and consumer purchasing power.

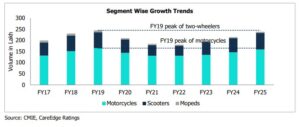

Segment-Wise Trends: scooters outpace motorcycles

The scooter segment continues to shine, registering double-digit growth for the third consecutive year. Sales rose 17% in FY25, following 13% growth in FY24 and 26% in FY23. Having already surpassed their pre-COVID sales levels, scooters are expected to outpace motorcycles in FY26, driven by rising popularity among urban commuters and women riders.

Motorcycles—still the largest segment—grew 9% in FY25, up from 8% in FY24. Entry-level motorcycles, once hit hard post-COVID, posted a modest 8% year-on-year growth, signaling the start of a recovery. Executive and premium motorcycle segments saw stronger gains of 12% and 10%, respectively, reflecting growing disposable incomes and evolving consumer preferences.

Motorcycles—still the largest segment—grew 9% in FY25, up from 8% in FY24. Entry-level motorcycles, once hit hard post-COVID, posted a modest 8% year-on-year growth, signaling the start of a recovery. Executive and premium motorcycle segments saw stronger gains of 12% and 10%, respectively, reflecting growing disposable incomes and evolving consumer preferences.

Although entry-level bikes account for 72% of total motorcycle sales, their share has declined from 75% in FY19—indicating a shift towards higher-value models.

“The executive and premium motorcycle categories are expected to lead growth in FY26, underpinned by stronger consumer sentiment and higher financial flexibility,” noted Arti Roy, Associate Director at CareEdge Ratings.

Electric two-wheelers gaining ground

Electric two-wheelers (E2Ws) remain a key growth driver, with volumes rising from 0.78 million units in FY23 to 1.20 million in FY25. Though growth slowed to 19% in FY25 (from 29% in FY24 and 180% in FY23), this was largely due to reduced government subsidies.

With incentives cut to ₹5,000 per vehicle—and expected to fall further to ₹2,500 in FY26—the focus is now on creating a sustainable EV ecosystem. The industry is shifting toward cost-efficiency, reduced subsidy dependence, and improved charging infrastructure.

Despite subsidy reductions, E2W demand continues to climb, thanks to lower operating costs and growing consumer awareness.

Regulatory Impact and export outlook

The implementation of OBD-II Phase-B emission norms in FY26 is expected to have a minimal effect on sales, with only a 1–2% increase in vehicle prices anticipated. Experts believe that improving affordability, a favorable monsoon, and rising incomes will help offset any adverse impact.

Exports, which made up 18% of total volumes in FY25, are projected to be a major growth engine in FY26. A 12–14% increase is expected as key African and Latin American markets recover from inflation and currency volatility.