{kind=link}

While quarterly performance remained robust across categories, June witnessed a 9.44% month-on-month (MoM) decline due to seasonal factors, liquidity concerns, and erratic weather patterns.

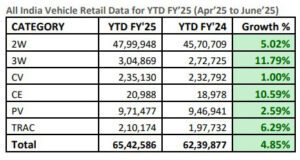

In Q1 FY26, all key segments recorded positive YoY growth: two-wheelers (2W) rose 5.02%, three-wheelers (3W) surged 11.79%, tractors grew 6.29%, passenger vehicles (PV) increased 2.59%, commercial vehicles (CV) inched up 1%, and construction equipment (CE) expanded by 10.59%.

FADA President C.S. Vigneshwar noted that retail sales in Q1 FY26 had aligned closely with the association’s projections. He acknowledged some early-cycle softness in the two-wheeler segment but expressed optimism about a strong recovery, citing seasonal demand and targeted strategies by original equipment manufacturers (OEMs) as key supporting factors.

Segment-wise trends in June 2025

In June this year, 2W sales grew 4.73% YoY despite a sharp 12.48% MoM drop, as festival and marriage-season demand cushioned the impact of financing constraints and variant shortages. PV sales rose 2.45% YoY but fell 1.49% MoM, with heavy monsoons and tight liquidity affecting conversions. Dealers also flagged rising inventory levels, which currently stand at around 55 days—partly due to compulsory OEM billing mechanisms.

The CV segment posted a 6.6% YoY increase, though volumes slipped 2.97% MoM. While early-month deliveries supported growth, new regulatory norms—such as mandatory air-conditioned cabins—added to ownership costs, dampening sentiment amid subdued infrastructure activity.

Meanwhile, CE showed remarkable strength with a 54.95% YoY and 44.98% MoM surge, driven by ongoing construction activity. Tractors continued their solid run, registering 8.68% YoY and 7.25% MoM growth, reflecting healthy rural demand.

Outlook: mixed sentiment amid rural optimism

The near-term outlook remains cautiously optimistic. Monsoon rains are forecast to exceed 106% of the long-period average (LPA), supporting rural consumption, especially for 2W and tractors. Early Kharif sowing, up 11.3% YoY to 262.15 lakh hectares, further bodes well for hinterland demand.

At the same time, robust government capital expenditure—particularly in roads, railways, metros, and green energy—is expected to buoy the CV and CE segments through the July–August period. However, risks persist from geopolitical tensions, rare-earth material shortages, and the potential spillover effects of US tariff actions on supply chains.

Dealer sentiment is currently skewed towards a slowdown, with 42.8% expecting flat sales and 26.1% anticipating de-growth. Booking pipelines remain muted, with only 21% of 2W, 38% of PV, and 32% of CV dealers reporting healthy enquiry flows.

Overall, FADA maintains a stance of cautious optimism. While rural tailwinds, festival preparations, and government spending signal promise, challenges such as heavy rainfall, elevated vehicle prices, supply-side constraints, and financing headwinds could limit momentum across key auto segments.