{kind=link}

Analysing the development of India’s energy sector since independence can be compared to looking at a half filled jar. Is it half full or half empty?

If we use a reasonable and not even an ideal standard, it has not been a satisfactory performance. One can even claim that it was a shameful performance, when more than 660 million Indians even today have to depend on non-commercial energy sources like firewood for cooking. Even after 40 years of independence, non-commercial energy sources contributed 43 per cent of India’s primary energy needs in 1987 and 20 per cent in 2021. Finally in 2019, 100 per cent of the households have access to electricity. But many households cannot afford power connection. We are yet to win war against energy poverty.

On the other hand, today, India is the world’s third largest energy consuming country. There are 314 million LPG connections in India which is almost most of the households in India. The country has been able to achieve two important goals of Nationally Determined Contribution agreed in 2015, to fight climate change crisis much before 2030 – cumulative electric power installed capacity from non-fossil sources to reach 40 per cent; reducing the carbon emissions intensity of GDP by 33 to 35 per cent compared to 2005 levels.

India’s energy production capacity

India’s total power generating capacity has increased from a meagre 1.4 GW at the time of independence to 410 GW at the beginning of 2023. India is targeting to reach power generation from renewables of 500 GW by 2030 – a remarkable achievement, if it happens. As of 31 January 2023, India’s installed renewable energy capacity (including hydro) stood at 168 GW, representing 40.9 per cent of the overall installed power capacity.

Oil production has increased from a mere 3.0 MT in 1965 to 34.0 MT in 2021 after reaching a maximum of 42.9 MT in 2011. Similarly, gas production was just 0.6 Billion Cubic Meters (BCM) and in 2021 it was 28.5 BCM after reaching a maximum of 47.4 BCM in 2010. On the other hand, coal production has increased every year from 130 MT in 1961 to 811 MT in 2021.

Most disappointing performance was in nuclear sector. It started with a meagre production of 0.7 TW in 1969 and reached only 43.9 TW in 2021. In 1962, forecast was to achieve 20,000 MW of nuclear capacity by 1987. Later, the same target was set to be achieved within the next 10 years. After 30 years, we have still not reached even 10,000 MW. Despite starting production only in 1993, China produced 408 TW in 2021. India’s hydro generation was 19.2 TW in 1965 and in 2021 it was 160 TW. Contribution from renewables was 172 TW in 2021 – a remarkable increase from 10 TW in 2005.

At the beginning of June 2023, coal and gas based power generation were 56.7 per cent of total installed power generation capacity while hydro, wind, solar and other renewables, 41.4 per cent. Nuclear contribution was only 1.6 per cent.

India’s oil consumption in 2022-23 was 222.3 MT and import dependency was 87 per cent. Import dependency for gas was 44 per cent. India’s total energy consumption in 2022 was 863 million tonnes of oil equivalent (MTOE) with a per capita consumption of 0.62 TOE. It was 2.68 for China, 6.79 for the US and average for the world was 1.36 TOE.

Access to energy increased

However per capita figures do not have much significance and is not an index of energy poverty. Energy requirements are often dependent on weather conditions. It is possible to have reasonable standard of living without consuming high level of energy.

It was only after allowing private sector in power generation in 1991, India’s power sector grew rapidly. Currently, private sector generates 49 per cent of the country’s thermal power, whereas states and the centre generate 25 per cent and 26 per cent, respectively. Availability of power in rural areas which was about 12:30 hours in 2015 has gone up to 21:09 hours and in the urban areas it has gone upto 23:41 hours. This has also significantly reduced consumption of kerosene from 892 crore litre in 2014-15 to 204 crore litre in 2020-21. This shows that more households are able to access electricity in recent years.

Poor management of distribution companies

Today, India has even surplus generating capacity. But supplying 24X7 quality power in most parts of India remains a dream. Because of populist policies of subsidised or free supply to agriculture sector, inefficient management structure of power distribution companies and frequent interference by the government in managing power sector, state distribution companies are in perennial loss position. Less said the better, about the corrupt practices and power theft.

In 1999, to streamline the operations of power sector and to put power tariff structure on scientific basis (to reduce political interference), autonomous and independent Electricity Regulatory Commissions were established. Unfortunately, they have not been able to function the way they were expected to, despite adequate training and facilities.

Since the financial conditions of distribution companies are precarious, they are unable to pay for power purchase from private companies. This in turn is affecting the entire power sector value chain. Despite the herculean efforts of the centre to put distribution companies on sound fiscal conditions, there has not been much progress.

Unfortunately because of the misinformed and misguided gas pricing policy of the petroleum ministry, natural gas industry has failed to develop. Needless to make the obvious point that when the ministry has to allocate critical commodity like gas under price control, there is ample rent seeking opportunities.

Some of the problems of petroleum sector could have been avoided or minimised if there were effective, and independent regulatory commissions staffed with honest experts and competent managers. Today, they do have sector regulators but they are just extension of the ministry without any independent power to prevent political interference.

Transition to net zero emission

In the past, during which peak oil was a problem, energy security was of larger concern. However now with peak demand, and the need for energy sector to decarbonise, bigger issue is not energy security, but how to plan for energy transition. Promotion of electric vehicles, use of hydrogen to handle intermittency of renewables, promoting battery storage and access to rare earth materials like lithium, cobalt, etc. used in renewables need to be focussed.

As India is aiming for net-zero by 2070, difficult choices have to be made about adding to refining capacity, coal power generation, oil exploration and production, natural gas supply infrastructure, etc. To make such strategic decisions, India needs the most competent experts with rich experience in energy sector. Where and how to find them?

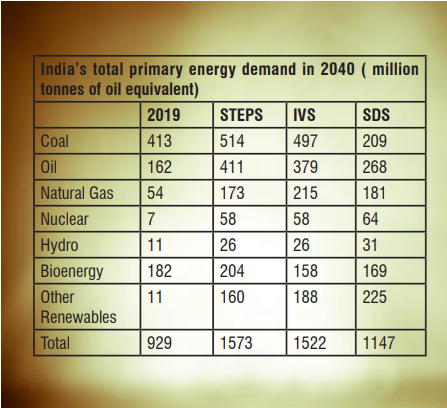

The complexity of the energy planning for the future can be illustrated through the three scenarios developed in IEA’s India Energy Outlook 2021 ( see table -1). Three scenarios are: Stated Policy Scenario (STEPS) is based on current policies and constraints, India Vision Scenario ( IVS) is based on the then prevailing Covid health situation being resolved and achieving faster economic growth with the stated policies, Sustainable Development Scenario (SDS) attempts to achieve net zero to progress towards achieving other sustainable development goals.

The complexity of the energy planning for the future can be illustrated through the three scenarios developed in IEA’s India Energy Outlook 2021 ( see table -1). Three scenarios are: Stated Policy Scenario (STEPS) is based on current policies and constraints, India Vision Scenario ( IVS) is based on the then prevailing Covid health situation being resolved and achieving faster economic growth with the stated policies, Sustainable Development Scenario (SDS) attempts to achieve net zero to progress towards achieving other sustainable development goals.

Table shows how widely the energy demand can vary depending on the unfolding of different energy scenarios. India’s total energy demand in 2040 could be as high as 1573 mtoe or as low as 1147 mtoe. Coal demand could fall to a low of 209 mtoe while oil and natural gas demand could increase to 411 mtoe and 215 mtoe respectively. It is such possible wide variations make the planning exercise extremely complex.

India also has a great opportunity to demonstrate to the world how to achieve net-zero by adapting the vision of Lifestyle for Environment (LIFE). India can be a shining example to the world by implementing its civilisational message of “simple living, high thinking.” India should give up the idea of maximising GDP, and instead adapt the goal of minimising poverty to facilitate quicker net zero achievement.