{kind=link}

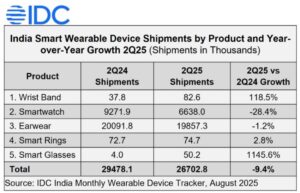

The sector also posted its fifth straight quarterly decline, with shipments down 9.4% YoY to 26.7 million units in 2Q25. The average selling price (ASP) of wearables saw a modest rise of 2.2% YoY to $19.2 in 2Q25, while remaining flat at $18.7 for the half year.

Smartwatch shipments continued their downward trend, declining for the sixth consecutive quarter. Volumes dropped 28.4% YoY to 6.6 million units in 2Q25, shrinking the category’s share of the overall wearables market to 24.9% from 31.5% a year ago. IDC attributed the slump to demand fatigue and saturation in the entry-level segment. Even advanced models struggled, with shipments falling 39.5% YoY. Despite the slowdown, ASPs rose 5.1% YoY to $21.7 in 2Q25.

The earwear category slipped marginally by 1.2% YoY to 19.9 million units. Within this segment, Truly Wireless Stereo (TWS) maintained its dominance with a 71.2% share, though shipments dipped slightly. Neckbands recorded a sharper fall of 16.1% YoY, while over-the-ear models bucked the trend, surging 97.4% YoY to 1.5 million units. The ASP for earwear grew modestly by 1.1% YoY to $17.4.

Among vendors, boAt (Imagine Marketing) retained its leadership in the overall wearables category, expanding market share to 28.0% in 2Q25. The brand posted strong gains in the over-the-ear segment, with shipments soaring 198.4% and capturing 44.4% share. In the TWS segment, boAt led with 31.9% share, followed by Boult at 14.9%.

In smartwatches, Noise (Nexxbase) held the top spot with 30.9% share, while boAt rose to second place at 13.7%. Xiaomi emerged as the fastest-growing smartwatch vendor, recording a 145.5% YoY surge in shipments.

Channel-wise, online sales dropped 13.8% YoY in 2Q25, pulling the channel’s share down to 60.3% from 63.4%. The decline was sharpest in smartwatches, where online shipments plunged 37.2%. Offline sales fared better, falling just 1.8% YoY, supported by a 4.4% rise in earwear shipments. Offline smartwatch sales also declined, but at a slower pace of 14.8%.

IDC expects the smartwatch market to witness a steep double-digit decline for 2025, citing regulatory pressures around local manufacturing and subdued consumer demand.

“Looking ahead to the festive second half, brands are expected to pivot towards mid-premium offerings, focusing on advanced health sensors, NFC support, AI-driven features, and ecosystem integration,” said Anand Priya Singh, Market Analyst, Smart Wearable Devices, IDC India adding, “White-label smartwatches are also likely to regain momentum in offline retail through aggressive bundle offers.”

Despite headwinds in traditional categories, emerging wearables showed early signs of adoption. Smart rings rebounded with 2.8% YoY growth to 75,000 units, led by Ultrahuman, Gabit and Aabo with a combined 65% share.

Smart glasses shipments surged to 50,000 units from just 4,000 a year earlier, driven by launches from Meta and Lenskart, with ASPs averaging $134. Smart wristbands also saw strong growth, with shipments rising 118.5% YoY to 83,000 units, largely fuelled by Samsung’s Galaxy Fit3, which accounted for more than 80% of the category.