{kind=link}

Reliance – the corporate Brahma… **Cover story**

by V.Ranganathan

The isa Upanishad opens with the following sloka in Sanskrit:

OM! POORNAMADHAH: POORNAMIDHAM POORNAATHPOORNAMUDHACHYATHE!

POORNASYA POORNAMAADHAAYA POORNAMEVAAVASHISYATHE !!

OM! SHANTHI: SHANTHI: SHANTHI:

OM! That (Invisible-Absolute) is whole; whole is this (the visible phenomenon); from the Invisible Whole comes forth the visible whole. Though the visible whole has come out from That Invisible Whole, yet the Whole remains unaltered. Om! Shanthi ! Shanthi! Shanthi !

At The End of each thousand chatur yugas the entire universe dissolves (prakruta pralaya), into the ONE absolute. And after a lapse of time the universe reappears from the ONE absolute. The phenomenon which is explained by the sages and seers but not experienced by any living person at any time, is something that can be perceived unfailingly in the evolution of the corporate behemoth, Reliance Industries Ltd!

The most recent restructuring of the group where the oil to chemicals (O2C) business is being spun off to a subsidiary in some sense signifies the reappearance of the universe after the last prakruta pralaya which in itself not a single event but a culmination of various sub evolutions and absorptions over the last about four decades. Just as the universe will continue to go through the dissolution and reappearance sequence, the latest perhaps is not the last of the metamorphosis of this incredibly vibrant company. But in size and implications this perhaps dwarfs anything else seen over the decades. The stakeholders responsible to approve this have put their seal just a couple of weeks ago and surprisingly the event didn’t draw the media attention and evaluation which many other less noteworthy corporate actions had attracted.

Reliance Petrochemicals Ltd. (RPL) Surfaces

Reliance Textile Ltd started as a textile business and set up its first foray into the petrochemicals through an outfit Reliance Petrochemicals Ltd and raised about Rs750cr from the public in 1987, a massive sum in that era. This company, while implementing the initial projects in chemicals, merged into the parent company effective 1 April 1992 and the shareholders of Reliance Petro were allotted 1 share in Reliance Textiles for every 10 share they had in Reliance Petro.

BIRTH AND DEATH OF ILLU AND PILLU

In 1992 the parent gave birth to a twin, illu and pillu (so affectionately named by the denizens of Dalal Street).

Reliance Polyethylene Ltd and Reliance Polypropylene Ltd, made identical public issues at a premium which was carefully hidden in the complex structure of the optionally convertible bonds. The twins dissolved into the parent in 1995 when the projects were still under implementation at the swap ratio of 25 shares and 30 shares of the parent for every 100 shares of illu and pillu respectively.

RPL re-appears in 1993

In 1993 the parent created a new progeny, Reliance Petrochemical Ltd (like the old time kings the same name keeps appearing in every new generation!) and a mega public issue raised money through what was then acclaimed the most fancy instrument, the triple option convertible bonds! The concept of a non convertible portion (khoka) being stripped and traded at a loss to claim it for tax purposes became a novelty that a few other Indian promoters readily embraced! In 2002 the life span for the off spring was over and at a swap ratio of 1 share of the parent for every 11 shares of the baby, the final rites were completed.

In all of the above creation and destruction, the promoters managed to augment their shareholding by innovative planning of treasury stock, which the law enacted in 2013 banned.

Reincarnation of RPL in 2006…

After a lull, in 2006 Reliance Petrochemicals Ltd reemerged as a fresh creation for an export oriented refinery and hit the market for a blockbuster issue of approximately Rs 2700 crore, an unthinkable sum then, at a hefty premium for a company that just had the licence to set up the project. Come 1 April 2008 the swap ratio of 1 share in the parent for every 16 shares marked the obituary of the new company.

O2C is being spun-off to a subsidiary in 2021

After a long life of creation and destruction at periodic intervals, witness now the emergence of the visible whole as stated in the Upanishad from the Absolute Whole on the appointed date of the latest scheme of arrangement being 1 January 2021!

The shareholders of Reliance Industries do not get any share in this spin off and the transaction is structured as a sale of business for settlement of consideration by the new O2C enterprise to the parent. The shareholders of Reliance will virtually hold a company that has no more any active business but just investments in O2C, telecom and retail. It is for the informed experts to debate if the restructuring mode adopted is to the benefit of the non promoter shareholders and how the independent board of Reliance agreed to this option and what alternatives were considered and overlooked.

It may be a reasonable inference that the company which has earned the moniker of ‘zero tax’ has pursued this option to not lose that distinction and preserve its mountain of MAT credit. And the unannounced amendment in the Finance Bill 2021 during the debate in the parliament to tax slump sale, prospectively, has perhaps ensured that the tax man poses no challenge to this scheme which has been made effective from an anterior date!

While the scriptures affirm that the ONE absolute appears as many to our perception, does the market respect this and value the WHOLE as the sum of parts?

| The tax savers

In the statement of profit and loss for 2019-20, the profit before tax shown by Reliance Industries was Rs 40,316 crore on a revenue of Rs 365,202 crore. Continuous investments on fresh projects helped the company claim large amounts as depreciation/amortisation expense. These amounted to Rs 9728 crore for 2019-20. Such financial management had enabled the industrial giant to keep tax outgo pretty low: for the year current tax was shown as Rs 7200 crore and deferred tax as Rs 2213 crore.  RIL’s PR spinners showed handsome figures for the decade 2010 to 2020 as contribution to national exchequer (Rs 54,842 crore for 2019-20). – SV |

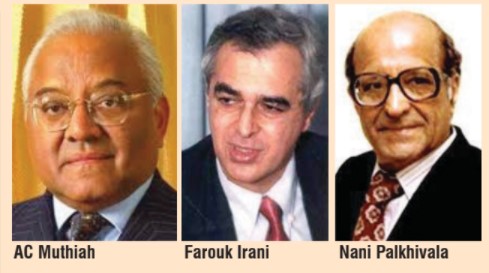

| THE Rise and fall of Leasing Industry…

The rise and fall of the leasing industry in India happened in a matter of a couple of decades. The rise is attributable to the benefit of capital allowances being captured in the books of the leasing company thereby minimizing the tax outgo together with faulty accounting practices. The fall was caused by gradual removal of tax incentives, introduction of minimum alternative taxes and the change in the accounting rules that necessitated a better matching of the income and corresponding capital charges.  Farouk Irani pioneered the concept in the mid 1970s and set up the First Leasing Company of India Ltd in association with SPIC Group’s A C Muthiah. Till then the business of lending was largely driven by the hire purchase model which was a security based lending. The ground for leasing became fertile with the tax law having major incentives for asset ownership used in the manufacturing industry. First Leasing capitalised on the fact that asset-intensive industry would normally have less appetite for tax allowances in the early years. By separating the ownership and usage, the arbitrage was fully exploited. The concept of matching the income from leasing with the right amortisation of the capital value was absent and the company law did not tune itself to this innovation and continued with nominal rates of depreciation on straight line basis. The companies started reporting very rosy post-tax profits and aided by a stock market that had very little transparency and weak audit oversight, the investors were milked for high premiums and the industry almost resembled a ponzi scheme. The assets chosen for leasing were also highly risky like film roles and scaffolding sheets due to the high depreciation allowed on these under the Income Tax Act. When tax authorities questioned the eligibility of the industry to allowances like investment allowance, N A Palkhivala appeared for First Leasing before the income tax tribunal in Chennai and secured the addmissibity of the tax benefit. However greed and over-trading by the industry and banks failing to monitor the rampant borrowing against non-existent assets or double financing the same asset, gradually led to market disillusionment. The change in accounting and tax laws finally rung curtains down on this industry which stands now discredited by the failure of some of the biggest names like First Leasing, Tata Finance and numerous other players. All this did not prevent the rise and seismic collapse of ILFS taking almost the entire economy down in its demise in 2017!! -VR ( The author is a CA and CS and retired as a partner at EY, Chennai.)

|

| Tax compliance…

“Once Anantharamakrishnan was going to pay Rs 75 lakh as corporation tax for one company alone. I told him that it could be diverted for some industrial research, some charitable or educational purpose. But Anantharamakrishnan said he will do it no doubt, but then it will not be at the cost of avoiding tax.” – R Venkataraman.  Anantharamakrishnan remained steadfast to his last in paying out correctly taxes that became due; but the era of tax planning unfolded much later in the 1970s when tax rates stiffened and incentives for investments expanded. Palkhivala and Dhirubai Ambani unfolded their grand designs of nil or low levels of corporate tax payments by conceiving and implementing year after year, large projects, the depreciation and incentives on which enabled the concerned unit to pay little or no taxes. Look at the record of TELCO in an era when it expanded massively: in the years 1975–76 to 1985–86 sales of TELCO increased from Rs 270 crore to Rs 1002 crore; profits before taxes for these 11 years amounted to Rs 212.03 crore; but Moolgaokar’s many-faceted expansion and Palkhivala’s tax planning limited tax payments to a paltry Rs 9.31 crore. In seven out of 11 years the company paid zero income tax! In the absence of the Simpson Group conceiving projects involving, at a time, sizeable investments, not much benefit had been derived by the group from the tax incentives that were liberally made available for encouraging investments. Right through the years when handsome investment allowances were available, the group derived little advantage. For 1989-90, for instance, the year in which Simpsons recorded a handsome jump in profits, the pay out by way of corporate taxes also increased steeply to Rs 2.17 crore from Rs 73.50 lakh for the previous year. Outgo in interest charges has also been sizeable – over Rs 3 crore for each of the two previous years related to a turnover of Rs 77 crore. While the group deserves the kudos for its sense of duty by the state, yet it may also be construed as an index of the inability to conceive and implement large projects that will help it save on taxes and plough back such savings into new projects. –SV (From IE August 1990 issue.) |