{kind=link}

An oft used expression from the past ‘The seven-year itch’, may look an awful anachronism. In that background, five years is almost an eon.

GST had a queer origin, its most strident critic, Arun Jaitley became its most ardent advocate post the change in electoral fortunes in 2014. From there on, it was a smooth cruise for the most momentous change in the fiscal architecture of the country ushered in July 2016.

The tax has grown from strength to strength with increasing collections and has greatly changed the way business is run in the country, with greater transparency and ease.

WHY GST?

GST became a necessity to address the multiple problems that business faced by the plethora of tax systems simultaneously operating in the country. GST can be credited with the following advantages:

GST became a necessity to address the multiple problems that business faced by the plethora of tax systems simultaneously operating in the country. GST can be credited with the following advantages:

(a) Elimination of tax as a cost on inter-state movement

(b) Integration of tax on goods and services

(c) A common data base of all business transactions

(d) Elimination of physical barriers like check posts

(e) Detection of frauds by electronic monitoring of movement of goods

(f) A uniform, common rate of taxes across the country

But to get here involved a wrenching alteration to the fiscal system.

The constitution was largely modelled on the predecessor Government of India Act 1935. This left little scope for raising revenues at the level of the provinces in the British India. The only crevice that was perceptible was taxing sale of goods; Madras Presidency under Rajaji took advantage and levied the sales tax.

Little changed when the country adopted its own constitution. Fiscal autonomy was little thought of except to mandate a finance commission to be set up every five years to work out the formula for sharing taxes.

In that light, the states giving up their sole lever to raise resources independently was a stellar sacrifice, may be in a sense short-sighted as well!

WHERE IS THE BUOYANCY IN REVENUES?

The only solace for such a transformative change can be a revenue buoyancy that lifts all the boats and expands the fiscal space to help spend more, which every politician cherishes – for peoples’ and their own benefit!

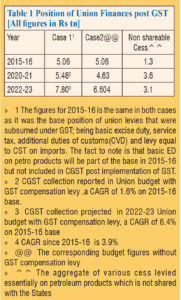

The euphoria in the media month after month when GST collection figures were announced seemed to indicate a major turnaround in the fiscal fortunes of both the Union and the states. But the numbers, when set in context, do not seem to validate the perception.

The euphoria in the media month after month when GST collection figures were announced seemed to indicate a major turnaround in the fiscal fortunes of both the Union and the states. But the numbers, when set in context, do not seem to validate the perception.

Table 1 shows that the CAGR in GST collection(including the cess) of the Union government since its inception in 2016-17 till the 2022-23 budget is a very modest 6.4 per cent and a more depressing figure of 3.9 per cent when the compensation cess is eliminated.

The GST figures have shown an increasing trend. the critical analysis is to see the growth over the original tax base when the government collected multiple taxes like Central excise, service tax, compensatory CVDs on imports … which were subsumed in GST.

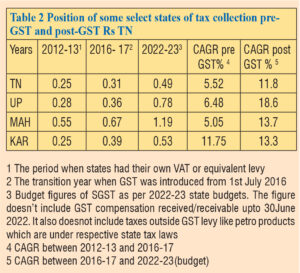

The effective collection under GST may have actually fallen when indexed for inflation and set against the actual GDP growth. This aspect may be seen in the data presented for a few select states in Table 2 and Table 3.

A state like Tamil Nadu has actually recorded a lower growth in GST over the five-year period as compared to the CAGR of the state GDP over the same period. The other states in the list, except UP, do not disprove this correlation.

GST changed the method of accruing taxes – it shed the origin-based system of the earlier of taxes, levies and became consumption or destination based. Producing states like Tamil Nadu and Maharashtra seem to have lost out to a state like UP with a large consumption base. Therefore, the fiscal gap may have actually increased, forcing these states to look for shoring up the finances by increasing the tax on petrol kept out of the GST compact.

SHOULD STATEs FOLLOW CENTRE IN REDUCING FUEL TAX?

This opens up the next most debated issue in the last few weeks. Should states reduce taxes on petrol because the Union brought down the levy?

Table 4 brings home the grim fact that the states, with the exception of UP, have a poor growth of SOTR, taking into account all taxes levied by the state. The CAGR seriously falls behind the state GDP growth showing the desperate situation these states faced on the fiscal front.

Table 4 brings home the grim fact that the states, with the exception of UP, have a poor growth of SOTR, taking into account all taxes levied by the state. The CAGR seriously falls behind the state GDP growth showing the desperate situation these states faced on the fiscal front.

The only choice for these states so affected is to curtail expenditure and face the wrath of the electorate!

The decision on how the Union and the states respond to the demand to reduce taxes depend on their respective fiscal capabilities; it is most illogical to demand linking one action to the other.

Some experts point to some states charging a higher tax on petrol than the Union. This ignores the fact that the Union has all the fiscal levers at its disposal while the states, none! In fact, the way the Central treasury milked the oil sector over the last few years can be seen in Table 1.

LOSS OF DEVELOPED STATES

Table 5 shows the dismal picture of how the progressive states which contribute significantly to the national economy receive a disproportionately small moiety of the taxes shared by the Union government under the directives of the Finance Commission.

The states can entertain no illusion to arbitrarily deviate from the GST straitjacket. The recent decision of the Court, which has been unduly sensationalised, may provide little added leeway to the states: the concept of GST needs total adherence to the system and any deviation can only result in disturbing and disruptive discordance.

CGST and SGST are two sides of the same coin and inseparable. The obvious interpretation of the constitutional mandate that the legislative stamp is a necessity to bring into vogue any recommendation of the GST Council, can only be triggered in the event of some oppressive action that disadvantages a minority of states than to support an errant or a rogue state to flout the structure unfairly. The legislative supremacy can be a shield to prevent a harm and not a sword to cause one!

The sustainability of the compact between the states and the Union needs to be nourished with a more balanced distribution of the taxation powers and not make the states depend on the largesse of the Finance Commission or of the Union budget.

ALLOT CGST FULLY TO STATES

ALLOT CGST FULLY TO STATES

A mechanism to fiscally empower the states can be by eliminating the CGST component in the intra-state transaction and attribute the entire tax to concerned state. For example, a 18 per cent levy which gets split as CGST 9 per cent and SGST 9 per cent can in entirety accrue to the state where the transaction happens. This is also logical as taxation of goods and services should be localised and reward the state where the activity takes place.

Will the above bankrupt the Central treasury? The data in Table 6 help bring out the fact that the entirety of the GST collections accounted in the Union budget is smaller than the taxes shared with the states as per FC directive. In other words, even if the entire GST collection is foregone by the Central government, it will still be solvent and its budget intact.

But this may put at a loss some states which have been receiving a lion ’share of the tax transfer by the Union budget. However, they would net the full GST arising in their state. An exceptional case of privation can be compensated like the way states were compensated for five years.

LEAVE TAX ON IMMOVABLE PROPERTY TO STATES

Another dimension which may take the discussion out of the GST compass is the possibility to transfer the right to tax income relating to immovable property to the states. The logic of keeping income tax as a Union levy is the complexity involved in taxing the income that arise in different states and finding a basis to attribute it to the respective states. However, no such debate would arise in the case of immoveable properties. Whether it is rental income, capital gains, inheritance of property or wealth, the locus of an immoveable property is indisputable. This may help rope in agricultural land into the tax net which is a major source of evasion now.